Carbon Before Biology

We're going to need a hell of a lot more sugar. Nobody has built the infrastructure to deliver it.

This piece is part of a series on the Bioelectric Tech Stack; the infrastructure layers that determine who wins in biotech. Every layer in the stack is ultimately an energy conversion problem. Sugar is no different.

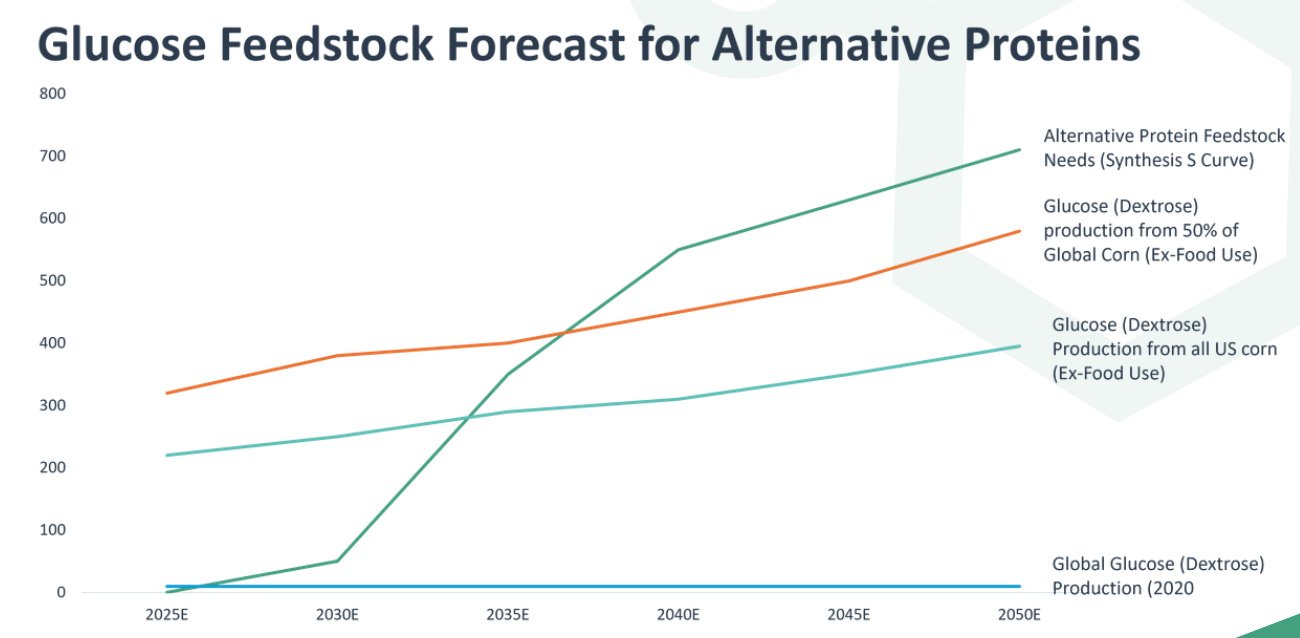

Figure: Glucose feedstock demand forecast for alternative proteins, 2025–2050. Source: FermBase by CREMER, From Grams to Global Supply Chains: The Hidden Scaling Reality of Fermentation (2026), adapted from USDA and Synthesis Capital estimates (2023). Projected alternative protein feedstock demand crosses available glucose supply from 50% of global corn production by the mid-2030s; and this is the alt-protein sector alone. Industrial fermentation for chemicals, materials, and fuels compounds the supply gap further. The bottleneck is not biological. It is agricultural.

Most people enter biotech through biology. They ask: which organism? which enzyme? which AI model? These are fair questions. But they are downstream questions. The constraint that actually determines whether a fermentation-based company lives or dies is further up the stack; it’s not about your organism, your enzyme, or your process. It’s about what you feed them.

Every industrial fermentation runs on the same basic formula: carbon plus minerals plus energy produces output. Carbon, in the form of glucose, sucrose, molasses, glycerol, or other feedstocks, is the primary input. Minerals round out the media. Energy drives the whole thing. Of these three, carbon dominates both cost and complexity. A recent article by FermBase puts carbon at 30 to 60 percent of total production cost in most fermentation processes, before you touch the bioreactor, before you hire a strain engineer, before you think about downstream processing. It is physical, geographically constrained, subject to agricultural cycles, and priced on commodity markets with limited ability to hedge. If carbon is expensive or unreliable, everything you build on top of it inherits that cost.

Carbon is the ceiling. And there are broadly four ways to change it. All four, at their root, are about making the energy embedded in biological systems go further.

The four ways to make carbon cheaper

1. Grow more carbon

The most direct intervention: make biomass cheaper at the source. Ultimately this is agtech. Every percentage point of yield improvement across a major crop reduces the system-wide cost of carbon for everyone downstream.

To understand the opportunity, we need to acknowledge the starting point. Crop protection is an oligopoly, BASF, Bayer, Syngenta, Corteva, with deep distribution relationships and decades of field data behind their products. For farmers operating on narrow margins with zero tolerance for crop failure, switching to unproven solutions is a significant risk. Reliable supply matters as much as efficacy. This makes market entry hard regardless of how good the science is.

Complementary technologies make for relatively rapid market entry as these work with the existing system rather than against it. Companies like Qarbotech (growth stimulants that increase solar yield from photosynthesis), Biostra (increasing water soil quality through water retention) and CDotBio (nanoparticle delivery systems that improve the stability and efficacy of whatever active ingredient they carry) are, in principle, compatible with conventional crop protection programmes. Farmers don’t have to choose, they can layer these on top of existing inputs. The risk is modest cannibalisation: if a biostimulant reduces stress sufficiently, a farmer might apply slightly less fungicide. But the primary value proposition is additive yield, not replacement. This makes the commercial path easier, even if the ceiling may be lower.

True replacements are harder and higher-stakes. Biobest, Vestaron and Enko Chem are building bio-based alternatives to synthetic pesticides and herbicides; molecules designed to displace incumbent chemistry, not complement it. BugBiome takes a related approach from a different angle; sourcing bioprotectants directly from the microbiomes of plants that have already evolved to resist the target pest. The science is credible, but the commercial challenge is significant: they are asking farmers to change behaviour, accept new risk profiles, and trust efficacy claims against products backed by decades of field data. Regulatory pathways are long and they are competing against companies with distribution relationships that took generations to build. The upside, if they get there, is that they will own a position in a market that has seen very little disruption.

Control technologies such as AI-driven sensing, automation, and precision application platforms like Prospera (crop monitoring) and Vivent Biosignals (plant stress detection via electrical signals), as well as direct intervention tools like Carbon Robotics (laser weeding) represent a different kind of intervention. Rather than changing the chemistry, they change the precision with which it is deployed: apply exactly what is needed, where it is needed, and waste drops. But conversations with experienced operators in this space surface a consistent constraint — the effectiveness of these technologies is often limited by their own energy costs. This is particularly acute in vertical farming, where artificial lighting, climate control, and automation stack up into energy bills that frequently overwhelm the productivity gains. The technology works. The unit economics are harder than they look.

Genetic modification, whether through conventional breeding, CRISPR, or more novel approaches, is the highest-leverage intervention and the longest-duration bet. Inari and Phytoform Labs are editing crops directly for yield traits, disease resistance, and input efficiency. The potential is significant: a crop variety that produces 15% more biomass per acre changes feedstock economics at a systems level. The challenges are regulatory, reputational, and commercial, distribution into a seed market that is itself highly concentrated.

Crops themselves are commodities and there is no venture return in growing corn. The return is in the enabling technology that makes crops cheaper, more productive, or less input-dependent. Every dollar saved at the field level compounds downstream through the entire fermentation supply chain.

There is also a policy tailwind that is easy to overlook. The Renewable Carbon Initiative, in work published by the nova-Institute, has made the affirmative case that using first-generation biomass for non-food applications can strengthen food security — by increasing overall feedstock availability, generating protein-rich by-products, and enabling rapid reallocation between food, feed, and industrial markets in response to supply disruptions. If the policy establishment is moving toward the view that directing biomass toward industrial applications is complementary to food security rather than a threat to it, the commercial and regulatory environment for this entire category improves.

2. Decouple carbon

The current industrial bioeconomy runs primarily on food sugars. That means carbon for chemicals competes directly with carbon for calories. When food prices rise — due to drought, geopolitical disruption, or energy shocks — input costs for fermentation rise with them. This is a structural vulnerability, not a temporary one.

There is a subtlety here that is easy to miss. Industrial biomanufacturing — producing chemicals, materials, and fuels — does not require the same feedstock purity as therapeutic biomanufacturing. A monoclonal antibody process demands highly refined, tightly specified glucose; contamination or variability at the sugar level propagates through to the product and ultimately to the patient. An industrial fermentation producing a specialty chemical or polymer has far more tolerance for feedstock variation. This matters because it opens up a much wider range of carbon sources — lower-grade sugars, molasses, partially processed lignocellulosic hydrolysates — that would be unusable in a GMP context. The opportunity is to exploit that tolerance deliberately, building processes that are designed from the outset around lower-quality, lower-cost inputs. The risk to avoid is the opposite: industrial biotechs that lazily source the same pharmaceutical-grade glucose as their therapeutic counterparts, competing in the same supply pool, driving up prices for everyone, and inheriting a cost structure that makes no sense for commodity-scale production.

China’s response is the most explicit. In 2023, six government departments led by the Ministry of Industry and Information Technology launched a dedicated three-year action plan for accelerating the development of non-food bio-based materials. The plan set out goals around saccharification technology, enzyme and strain libraries, and demonstration-scale production lines using non-food biomass, with companies like Henan Qiye already building facilities to process corn-based cellulose and lignin into fermentable sugars. The direction of policy is unambiguous: China intends to build an industrial bioeconomy that does not depend on food crops, and it is committing institutional resources to do so.

The private-sector decoupling agenda runs in parallel. LanzaTech uses industrial waste gases as the carbon input entirely, bypassing agricultural feedstocks. Companies working on lignocellulosic conversion, Novonesis among them, are trying to turn agricultural residues into fermentable sugars. Glycerol and molasses, by-products of existing food and fuel production, remain underutilised carbon sources that could serve more of the market if supply quality and logistics were better standardised.

The important nuance holds across all of these approaches: waste carbon is only useful if it is consistent, predictable, and cost-competitive. Most waste streams today are none of these things: geographically dispersed, compositionally variable, and contractually informal. Infrastructure-scale carbon conversion is capital-intensive and margin-thin. The national programmes create the policy tailwind; they do not solve the commercial problem. The venture-scale opportunity, as with agtech, is in the enabling technology, the tools that make conversion possible, or the platforms that aggregate, standardise, and coordinate supply.

3. Move carbon better

This is the most underbuilt layer in the whole stack.

Carbon is physical. It cannot be shipped as a file. A ton of glucose syrup is dense, heavy, perishable to some degree, and subject to logistics economics that have nothing to do with biology. Moving from lab scale to commercial scale in industrial biotech means moving from grams to tons to global supply and that transition exposes every fragility in the supply chain.

Most fermentation companies today operate with single-supplier relationships and informal procurement. They buy from one or two distributors, price on spot markets, and carry minimal inventory. This works at small scale. It fails badly when you try to grow. The large integrated suppliers (e.g. FermBase by CREMER) serve this market, but without the digital coordination layer that would make procurement efficient (yet). Aggregation platforms for fermentation-grade carbon are mostly absent. Preprocessing and densification tools (which would allow lower-quality biomass to become usable feedstock) are early and adjacent. Digital marketplaces for carbon trading in the bioeconomy are essentially non-existent.

This is not a logistics problem. It is a coordination problem. And coordination problems, when solved at scale, are worth a great deal.

The analogy is what enterprise resource planning software did for manufacturing supply chains in the 1990s; not moving the goods, but coordinating the information about goods well enough that the whole system became more efficient. A “carbon ERP” for the bioeconomy, sitting across agricultural suppliers, preprocessing facilities, logistics networks, and biomanufacturers, would have structural value far beyond what any single feedstock producer could capture.

This layer is almost entirely unbuilt. Loamist launched in 2024 with a biomass discovery and access tool (essentially a search layer for feedstock availability) before pivoting to trade finance AI. That pivot says something honest about how hard it is to build a business on top of a market that doesn’t yet have the volume or standardisation to support a coordination layer. Ecostrat has developed feedstock supply insurance and biomass zone ratings to de-risk supply chains for project finance. There is no funded, scaled company that owns the coordination layer across fermentation-grade carbon supply. The space that a mature carbon OS would occupy is genuinely empty.

And the feedstock layer is not the only one that needs building. Fermentation startups have raised billions in the last decade but remain unable to access industrial-scale production capacity across Europe and the US; a manufacturing gap the European Commission has identified as one of the sector’s most critical bottlenecks. This creates a classic chicken-and-egg problem: carbon coordination infrastructure is hard to justify without guaranteed demand from scaled biomanufacturing, and scaled biomanufacturing is hard to justify without reliable, cost-competitive feedstock.

The two sides of the stack have to be built together and the paths that have resolved this kind of stalemate elsewhere are instructive:

Shared infrastructure models distribute the capital cost across multiple users. Public anchor investment de-risks the first movers on both sides; Europe’s Circular Bio-based Europe Joint Undertaking, a €2 billion public-private partnership, is already deploying capital on exactly that logic.

Large agricultural corporations like Cargill have simply vertically integrated by building biology capabilities on top of feedstock infrastructure they already own, treating carbon supply as a strategic moat rather than a procurement function.

In China, the same logic plays out differently. Founders operating inside the ecosystem tell me that large companies buy directly from farming collectives, a procurement relationship that the structure of Chinese agriculture makes possible in ways that have no Western equivalent. The coordination problem doesn’t get solved; it doesn’t actually arise in the same form in the first place.

The Western startup ecosystem has no equivalent answer, it cannot vertically integrate its way out of a problem it doesn’t have the balance sheet to solve unilaterally. Which is part of why the fourth path may matter most, a biokeiretsu, a deliberately constructed cluster of feedstock, infrastructure, and biomanufacturing companies bound together through shared ownership and long-term offtake relationships, coordinating across the stack not because a market tells them to, but because they’ve built the incentive structure that makes coordination the rational choice.

4. Use less (briefly)

Strain engineering, process optimisation, and fermentation yield improvement all reduce how much carbon is consumed per unit of output. This matters, and the field has made significant progress. But it has limits.

You can halve your carbon consumption through years of strain development. You cannot engineer your way out of a feedstock that costs twice as much as it should, or one that disappears because of a supply disruption. Efficiency is a multiplier on feedstock economics — not a substitute for them.

Strain engineering and process optimisation could fill a series of articles on their own (and they will come!).

On minerals

Minerals are a separate constraint from carbon, and they follow a different logic. The intervention surface is narrower. You cannot grow more cobalt the way you can grow more corn, but the supply risk is just as real, and the venture opportunity is emerging faster than most fermentation companies have noticed.

At industrial scale, nitrogen, phosphorus, and trace elements become both a meaningful cost line and a potential supply constraint, particularly when procurement is treated as a purchasing function rather than a strategic one. Nitrogen is probably the largest molecular requirement behind carbon. Synthetic nitrogen fertiliser is energy-intensive to produce and exposed to geopolitical price swings, which is precisely why Pivot Bio‘s work on microbial nitrogen fixation is relevant here as much as it is in the agtech section. Cheaper nitrogen means cheaper fermentation media.

The more structural concern is that several minerals fermentation depends on (manganese, cobalt, nickel, zinc, copper, phosphorus) are the same ones the clean energy transition is racing to secure. Across the critical minerals fermentation depends on most supply is heavily concentrated in two or three countries, with China dominant in refining even where it doesn’t lead in extraction. The bioeconomy is not large enough to move these markets but it will feel them move.

The same biotech logic being applied upstream in fermentation is now being applied to mineral extraction itself. Companies like Endolith (AI-guided microbial selection with on-site bio-hatcheries) and Transition Metal Solutions (developing prebiotics for copper mines) are using engineered and enhanced microbial communities to unlock copper and other critical minerals from low-grade ores and tailings that conventional mining ignores: waste streams that often contain exactly the critical minerals that fermentation media depends on. RemePhy, a 2024 Imperial College spinout, takes a different route by engineering the symbiosis between metal-hyperaccumulating plants and soil bacteria to pull heavy metals from mining-contaminated land, with the harvested biomass then processed for metal recovery. Their primary pitch is remediation, but the phytomining application targets nickel, cobalt and manganese directly.

What’s notable about all three approaches is that none of them are attacking the mining industry, they’re enhancing it. Transition Metal Solutions feeds the native microbial communities already living in heap leach piles, RemePhy cleans up contaminated land that mines are already liable for, and Endolith integrates directly with existing heap leach operations. The value proposition in each case is more metal from the same rock, with lower chemical inputs and smaller waste streams, a much easier sell to a conservative industry than asking it to rebuild its infrastructure from scratch. The economics follow from that logic: Transition Metal Solutions estimates that a 5% improvement in leaching efficiency can be worth $100 million per mine annually, which means marginal biological optimisation at scale is a very large number.

The investment sequence

Putting it all together:

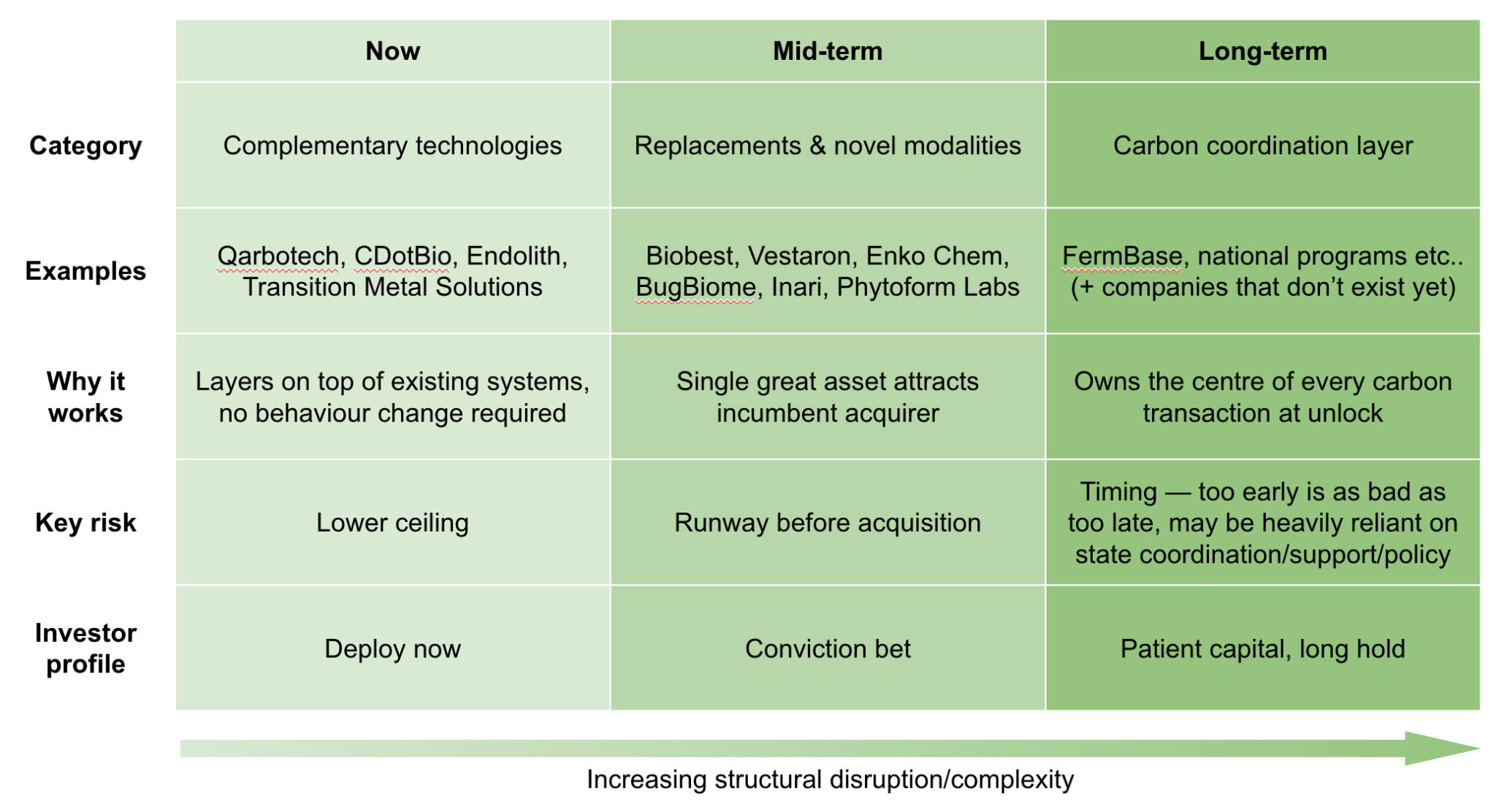

The near-term opportunities are in complementary technologies: the companies that make existing systems more productive without asking anyone to change behaviour. Growth stimulants, nanoparticle delivery systems, biomining players enhancing heap leach operations that mines are already running. These companies don’t need the market to mature around them. They layer on top of what already exists, adoption friction is low, and the value proposition is additive. For investors looking at the feedstock stack today, this is where the risk-reward is clearest.

The mid-term bets are in true replacements and novel modalities: bio-based crop protection, GMO varieties, entirely new feedstock pathways. The commercial path looks long if you assume these companies have to build their own route to market: regulatory timelines, farmer behaviour change, distribution relationships built over generations. But that assumption may be wrong. A company that establishes a single great asset in principle becomes an acquisition target at any point in its development and an incumbent with distribution can accelerate adoption in ways the startup never could. The science leads; the incumbents close. The timing is theirs to determine, not the market’s.

The longest and most structurally complex bet is the carbon coordination layer. It requires sufficient standardised supply on one side and sufficient scaled biomanufacturing demand on the other before there is anything worth coordinating. That stalemate breaks when one of several things happens: state coordination creates the demand signal at sufficient scale, a corporate with deep enough pockets decides the infrastructure is strategically necessary and builds it unilaterally, or a biokeiretsu emerges that bootstraps both sides simultaneously inside a structure that makes coordination the default. Which of those comes first is an open question. But the company that owns the coordination layer when the stalemate breaks will sit at the centre of every carbon transaction in the bioeconomy.

The three tiers demand different things from an investor. The complementary technologies are investable now. The replacements require conviction that the science will find a buyer before the runway runs out. The coordination layer requires patience and a view on what breaks the stalemate and a willingness to be early to something that cannot succeed until the conditions around it are ready. Each demands a different fund structure, a different hold period, and a different theory of value creation. The feedstock layer will get built. But the company that ends up owning the most valuable piece of it may not look like a biotech company at all, it may look like the infrastructure business that everyone else in the stack depends on.

you missed the biggest lever! plants themselves can be genetically engineered to make the desired chemical directly. Elo Life Systems is one of many molecular farming startups taking this approach.